Tyler Payne

Tyler Payne is a turnaround professional with experience in strategic transactions, refinancing, modeling and budgets, and business intelligence. He has four years of experience serving as a distressed creditor as well as four years of experience working as an operator within cash-constrained businesses.

David Tiffany

David Tiffany is a corporate finance and accounting professional offering over 20 years of leadership experience.

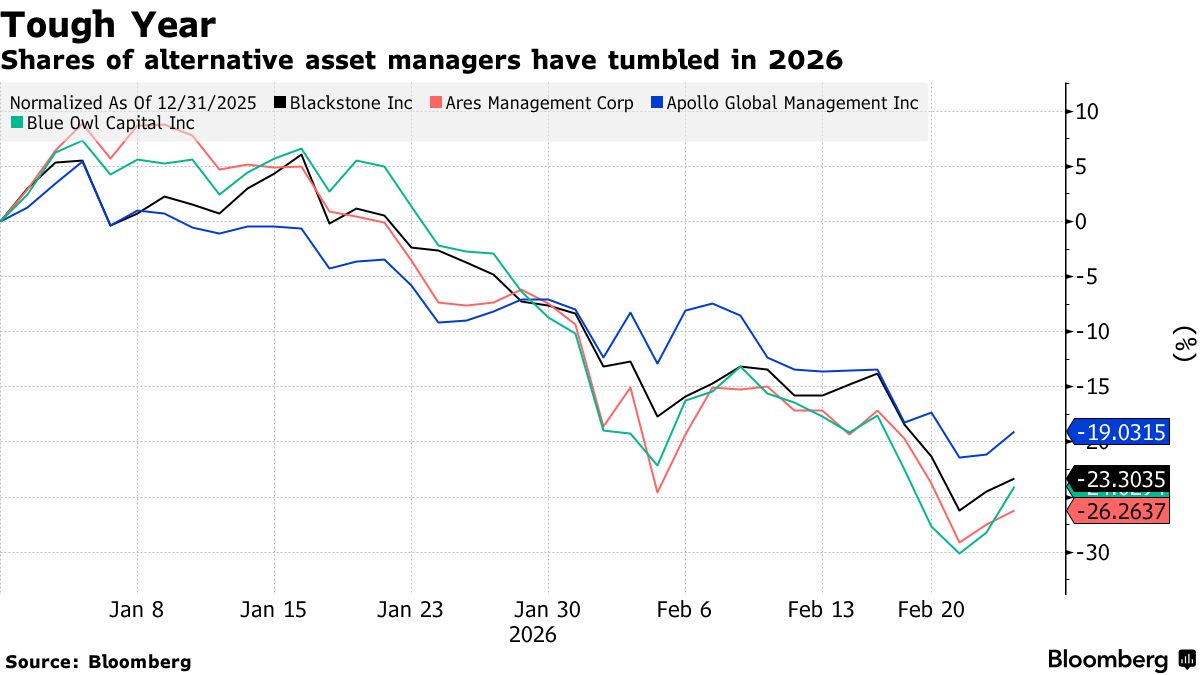

The meteoric rise of private credit over the past several years has some professionals in the restructuring industry’s spidey senses tingling after living through the mortgage crisis of 2008. Recently, rumblings in the market have occurred related to companies like Blue Owl who announced they were halting quarterly withdrawals in one of their funds effectively going into runoff, BlackRock limiting withdrawals, JP Morgan tightening credit to private credit and other large private credit institutions experiencing heavy redemptions. And many analysts and experts fear possible systemic risks from loans to software companies and their exposure to advancements in AI. In fact, it has been a tough year for many asset managers prominent in this space. But not all funds are created equal, and many have stuck to strict, disciplined performance.

Private credit is an asset defined by non-bank lending where the debt is not issued or traded on the public markets. "Private credit" can also be referred to as "direct lending" or "private lending" and is a subset of "alternative credit," therefore considered a relatively broad asset class.

Of course, there are different borrowers and lenders that likely do not involve the levels of fraud that it appears the mortgage situation may have included. Regardless, something about it feels similar.

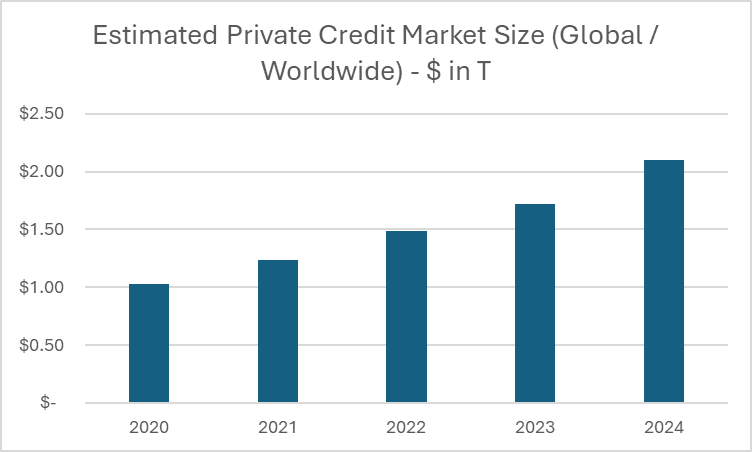

Private credit has become one of the most powerful, and least scrutinized, forces in global finance. Once a niche strategy centered on middle-market loans, the asset class now funds everything from leveraged buyouts to large corporate refinancings. Fueled by investor demand for higher yields and by regulatory constraints on banks, private credit has grown into a multi-trillion-dollar ecosystem.

However, behind the sector’s rapid expansion lies a shift in underwriting discipline. Covenant-light structures, compressed due diligence, and opaque reporting have become commonplace. These trends raise uncomfortable echoes of the dynamics that preceded the 2008 mortgage crisis, not because private credit resembles securitized mortgage-backed securities, but because the structural incentives and risk blind spots occurred prior to 2008 and we appear to be seeing that again.

1. The Explosive Growth of Private Credit

Private credit has tripled over the past decade as investors, from pension funds to sovereign wealth funds, have poured capital into the space in pursuit of stable, high yields. With so much dry powder to deploy, managers face pressure to put money to work. Borrowers, particularly private equity sponsors, are using that leverage to negotiate borrower-friendly deals.

- “Private credit” in this graph includes direct lending and other non-bank/private debt fund structures.

- Estimates vary depending on how “private credit” is defined as some include only closed-end funds, others also include listed funds, middle-market CLOs, semi-liquid, and open-ended structures.

- Data for 2023 and 2024 come with some lag and uncertainty, e.g. 2023 number is as of mid-year.

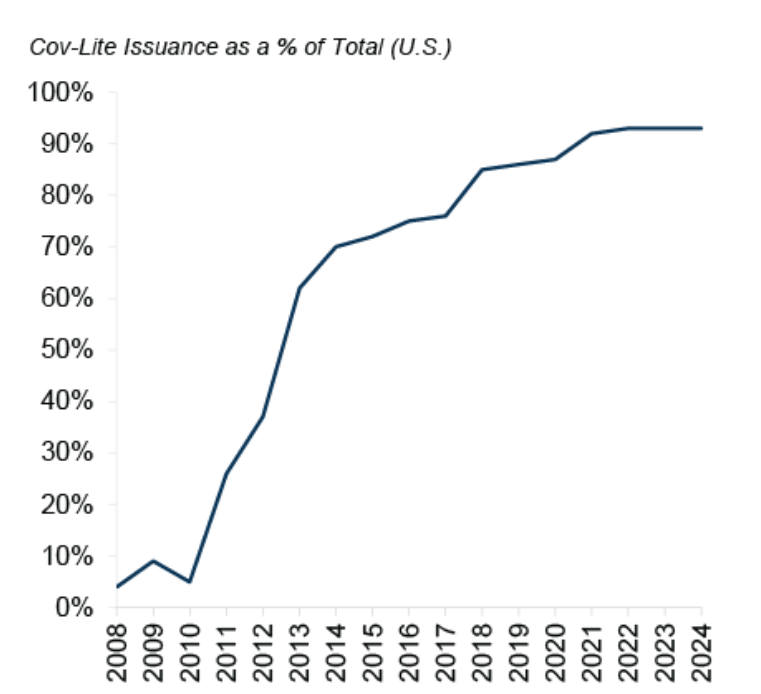

2. The Decline of Lender Protections

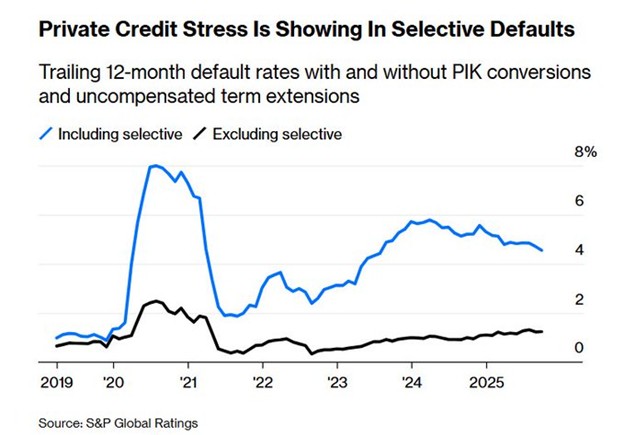

Covenants, especially maintenance covenants that require the borrower to continuously satisfy specific financial tests at regular intervals, are designed to serve as early warning systems. These early warning signs trigger corrective action before a borrower’s financial problems become irreversible. Yet today’s private credit market increasingly resembles the syndicated loan market of the late 2000s: covenant-lite, borrower-friendly, and light on accountability.

The result is that lenders may not be able to intervene until a borrower is already in distress, limiting recovery prospects and heightening default severity.

Common features now include:

- Fewer or no maintenance covenants

- Greater flexibility to incur additional debt

- Looser EBITDA adjustments

- Fewer reporting requirements

- Lender rights pushed deeper into default territory

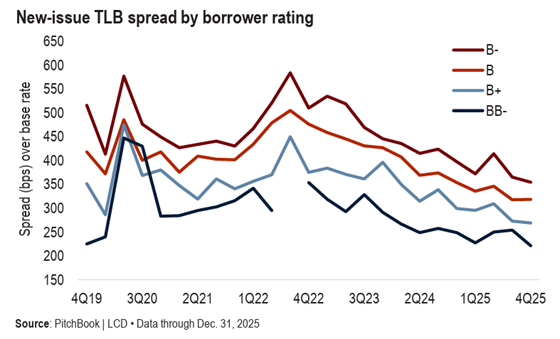

3. Compressed Due Diligence and the Competition Problem

As competition intensifies to deploy record high levels of capital, private lenders face pressure to move quickly, sometimes within days, and rely more heavily on sponsor-provided data.

Market participants report:

- Abbreviated financial reviews

- Reduced third-party analysis

- Less time to validate assumptions

- Faster auction processes that reward speed, not rigor

This creates risk layering: high leverage on top of optimistic underwriting with thin lender protections. Some say this is comparable to the days of the mortgage crisis when mortgage banks would modify their underwriting and rate sheets to “create” new products that would qualify with less rigorous diligence qualification requirements to complete loan syndication pools. Subsequently, underwriting certainly tightened significantly because of the lessons learned after the mortgage crisis.

4. Transparency: The Hidden Vulnerability

Unlike public markets, private credit has:

- No standardized reporting

- No price discovery

- No external rating requirements

- No secondary market depth

Many investors rely on quarterly reports that reflect manager-marked valuation, which may lag in reality, especially when covenants no longer flag early deterioration.

5. How This Mirrors the 2008 Mortgage Crisis

Private credit is not a repeat of subprime mortgages, but the underlying mechanics of risk buildup look familiar:

- Investors chasing yield → pressure to originate: The flood of capital into mortgage-backed securities pushed originators to loosen standards then. Today, massive inflows to private credit push lenders to accept weaker terms.

- Erosion of underwriting discipline: “No-doc loans” then, compressed diligence now. Different instruments, same incentive pathology. Looser structures hide true performance. Teaser rates and adjustable mortgages masked borrower weakness then, covenant-lite terms delay stress signals today.

- Opaque risk and delayed loss recognition: Ratings models and securitization hid mortgage risk pre-crisis then. Unwillingness to mark the value of the investment to market and limited reporting obscure credit deterioration now.

- Assumptions of diversification that may break into a downturn: Housing defaults became correlated in 2008. Private credit exposures, especially to sponsor-owned, highly levered companies, could correlate sharply during an economic slowdown. In addition, many funds are highly concentrated in software related companies.

6. Why This Looks Like 2008

Why This Looks Very Familiar

- Leverage is high.

- Underwriting discipline is weakening.

- Risk is hidden inside private structures.

- Investor demand encourages volume at the expense of quality.

Why This Is Not the Same Risk

- Private credit is not securitized at remotely the same scale, but does exist in recent distressed companies, including First Brands, Tricolor, and FAT Brands.

- Losses would likely be contained within institutional portfolios and loans to specific borrowers.

- Borrowers are companies with real operations, not households.

Conclusion

The systemic risk appears to be lower than in 2008, but the investor risk and portfolio concentration risk may be higher than most allocators appreciate.

7. What Happens When the Cycle Turns?

Although rates have begun to decline, when interest rates remain high or economic growth slows, the weaknesses in private credit will not remain hidden:

- Defaults will increase, especially among highly levered sponsor-backed borrowers.

- Recoveries may be weaker, because covenants no longer force early intervention.

- Valuation will adjust suddenly, not gradually, as lenders are forced to acknowledge deteriorating credit.

- Correlation will spike, undermining assumptions of diversification.

Private credit could experience a slow-burning, prolonged stress period rather than the sudden collapse seen in mortgage-backed markets, but the damage to investor portfolios could be substantial.

8. What Lenders and Investors Must Do Now

To navigate these risks, market participants can take several steps:

- Reinstate key maintenance covenants and reporting requirements

- Extend diligence timelines and reintroduce independent analysis

- Stress-test portfolios under scenarios of correlated distress

- Demand clearer disclosure and valuation transparency

- Monitor sponsor behavior, especially add-on acquisitions and dividend recaps

Conclusion

The private credit market’s explosive growth reflects genuine strengths: flexibility, speed, and access to capital for companies that might otherwise struggle to borrow. However, its vulnerabilities, weak covenants, fast-track underwriting, and limited transparency, are real, and echo the incentive failures that preceded the 2008 mortgage crisis.

Again, there are some very proven private lenders that have been in business a long time and will continue to do so, but the question is not whether private credit will face a reckoning. It is when and how prepared lenders and investors will be when the cycle turns.

About CR3 Partners, LLC

CR3 Partners, LLC is a national turnaround and performance improvement firm that assists, guides, and collaborates with management teams and their constituents facing any sort of transition, opportunity, stress, or distress. David Tiffany is a Managing Director and Partner based in Los Angeles. Tyler Payne is a Manager based in Los Angeles.